Retrofits are all the rage these days. From talk of climate action-oriented COVID-19 recovery strategies, to the recognition that many of our older buildings are ill-adapted to current conditions (particularly notable during the recent tragic heatwave), the problem of retrofits occupies the minds of many a business leader and policymaker.

The scale of the need for retrofits, from an economic perspective, should be enough to give anyone pause. Analysis from the Pembina Institute in mid-July showed that “a renovation wave of decarbonization retrofits over the next 20 years could create up to 200,000 long-lasting well-paid jobs, generate more than $48 billion in economic development each year [across Canada], create significant savings in healthcare costs, and pay for themselves twice over through increased tax revenue.” This would require somewhere near $15 billion per year for residential buildings, and another $6 billion for commercial and institutional ones.

The scale of both the opportunity and the spending need are immense. It’s why the Government of Canada, the Province of British Columbia, and innumerable local governments are ramping up incentives and working towards new forms of innovative financing programs, like Property Assessed Clean Energy (PACE) Financing. In Budget 2021, Ottawa provided $4.4 billion to the Canada Mortgage and Housing Corporations (CMHC) to help homeowners complete deep home retrofits through interest-free loans worth up to $40,000.

Even before that announcement, however, CMHC was working to develop a sustainable finance framework that would lay out its approach to climate action in Canada.

A centerpiece of that announcement was the interest in sustainable mortgage-backed securities (SMBS)

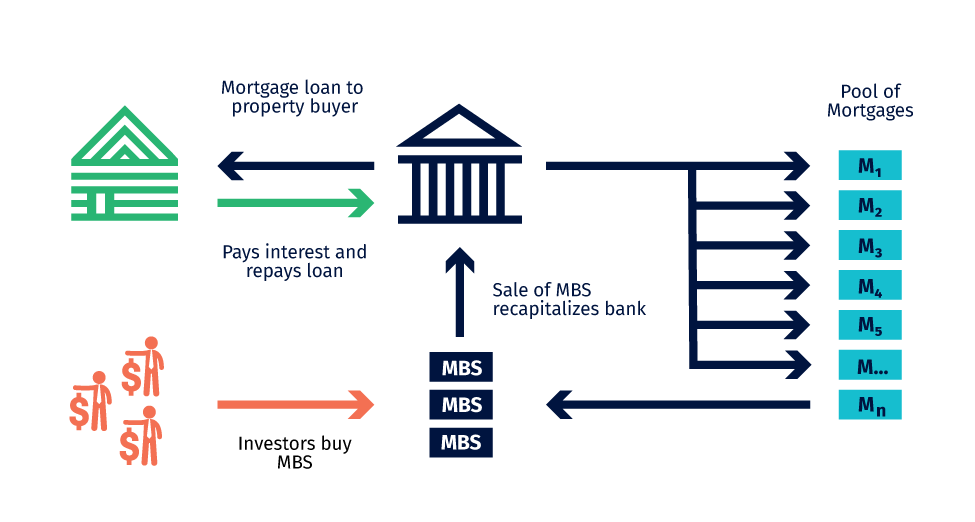

A mortgage-backed security is a pool of mortgages that have been brought together in a bond and sold to investors. Broadly speaking, they include Commercial and Residential Mortgage-backed Securities (CMBS/RMBS), which are backed by those respective property types.

Mortgage-backed securities explained

Source: Invesco: Mortgage-backed Securities and their functions

The general advantage to creating some kind of MBS is that it allows a bank to refresh its internal cashflows by selling the pooled mortgages to investors as a bond, and then use the money raised to fund more loans. In a capital-constrained economy, this can be very helpful. For investors, this can also be attractive as it allows them to get access to investments – like residential mortgages – that have an attractive risk or profit profile that might otherwise be unavailable to them. Their disadvantages include the potential for early repayment, which can make their long-term profitability unclear, and the somewhat opaque relationship that emerges between investors and borrowers through the securitization process.

A sustainable mortgage-backed security is the exact same mechanism, with the added layer of filtering and bundling mortgages on the basis of various measures of sustainability performance. For example, mortgages might only be included in the SMBS if they have an obligation and credible plan to reduce greenhouse gas (GHG) emissions by a certain amount over time.

SMBS are most popular in the United States, where the Federal National Mortgage Association (“Fannie Mae”) is the primary issuer. Fannie Mae uses its financial powers to maintain liquidity in mortgage markets by buying individual mortgages from lenders and packaging them into bonds, or by buying other MBS’ directly from banks.

In 2020, Fannie Mae issue nearly $88 billion (USD) in Multifamily SMBS and $94 (USD) million in Single Family SMBS (the latter having started that same year). This makes Fannie Mae the single largest issuer of green bonds in the world.

CMHC’s sustainable finance work, and the research underpinning it, see similar opportunities for SMBS in Canada.

Building on the work of VEC’s Commercial PACE and Resilience Report, VEC undertook a short research project to understand the potential role of SMBS in advancing retrofit markets generally, and what they might mean in the Vancouver context. With the Climate Emergency Plan, we have one of the highest-potential markets in the country – so, the interest in these kinds of new approaches is definitely high across many commercial and governmental actors.

The results, as our analysis shows, are inconclusive at best. While the Deloitte report for CMHC highlights that SMBS can help streamline market adoption of Environmental Social Governance (ESG) criteria across investing, the specific contribution to advancing retrofits is much more tenuous.

As BC has found even with its quite generous incentives, limited numbers of people are able to, or interested in, the types of retrofits likely to reduce emissions. The Canada Infrastructure Bank has struggled to get its $2.6 billion in retrofit financing out; and some critics maintain that it is simply lending to large property owners who would have made these investments anyway. As if the general problems with uptake weren’t enough, even with substantial government announcements, a supply of sufficiently trained contractors and equipment remain significant challenges as Vancouver’s and Canada’s construction forces age and struggle to attract talent.

Addressing the retrofit need will be one of our region’s most critical tasks in the next decade if we expect to meet our climate goals of 45-50% reductions in GHGs by 2030. It also, if done correctly, could be one of the single largest social and economic boons to our region in recent memory – creating new jobs, healthier spaces, and protecting against future climate shocks, like the “heat dome” in early July.

VEC believes the “retrofit economy” will be a significant part of our economy future, and is dedicating significant work to it, such as: